What is Financial Literacy?

Financial literacy is the ability to use skills and knowledge to take effective and informed money-management decisions. For India, financial literacy and awareness on financial opportunities is vital to promote financial inclusion and ultimately financial stability.

The Objectives of Financial Literacy:

- To inculcate habits of savings

- To help people in financial planning /household budgeting

- To help /build capacity and ability to borrow loan from different financial institutes/banks

- To understand and plan family budgeting

- To understand savings and options

- To understand investment and options

- To understand banking and different aspects

- To understand financial aspects in Loan

- To understand loan capacity

- To understand debt management

- To sustain financial growth by linking with income generation activities and self-help groups

Important definition and terms

-

Income:

Money earned from various sources like salary, wages, earnings or profit from farming, business, investment etc. is our income.Income Rs. (Amount) Salary of husband 10000 Salary of Wife 3000 Pension of father 2000 Earning from agriculture sale 4000 TOTAL INCOME 19000 -

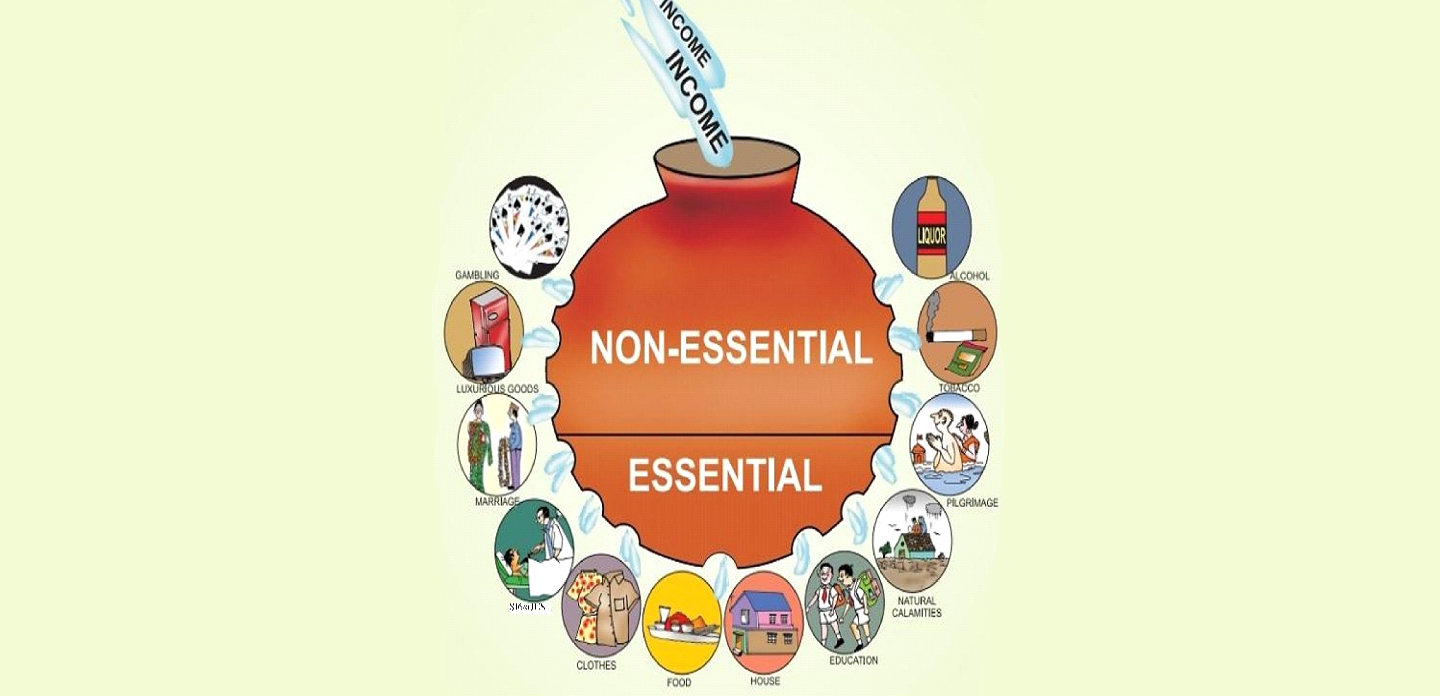

Expenditure:

Money spent on essential and non-essential items is expenseExpense Rs. (Amount) Food, shelter, Clothes 10000 Education 2000 Repayment loan 2000 Sickness 1500 Drink, drugs, Gutka 1200 Excessive expenses on Marriage, Festivals, Pilgrimage etc 500 17200

Let’s understand what’s essential and non-essential expenses through the poster above:

Central and State Health schemes

-

Aswasakiranam

-

Cancer care for children

-

Thalolam

-

Sruthitharangam

-

-

Snehapoorvam

-

Samaswasam 1

-

Samaswasam 2

-

Samaswasam 3

-

Assistance for Differently Abled

Medical Certificate and ID card

-

Special Assistance for Differently Abled through District social welfare office

-

Assistance available through Scheduled Caste Development Department

-

Snehasparsham for unwed mothers

-

Assistance under Kerala Tree Climbing welfare Scheme

-

Society for Medical Assistance to the poor

-

-

Rashtriya Arogya Nidhi

-

Karunya Benevolent Scheme

-

Samagra Arogya Insurance Scheme (RSBY & CHIS)

-

Janani Suraksha Yojana

-

Janani Shishu Suraksha Kaaryakram

Conclusion

As a humble step towards assisting the disaster-o//ected familiesin the state to rebuild their lives fromthe ground up in terms of Shelter, WASH, Finance Literacy and Disaster Management, the Habitat for Humanity India together with the Center for Disaster Philanthr Py implemented Housing Support Service (HSS) as a post disaster response in Paravur Taluk of Ernakulam District.

Through HSS, as envisaged, we delivered documentation and technical assistance as well as

planning and designing of sustainable construction methods for familiesin the area to reconstruct their homes which were shattered

by the unprecedented flood in 2018. In time to come, HSS could be considered as a scaling strategy serving amilies without directly

involving in the construction of houses.

In light of the need for creating a resilient pathway or the

families,a comprehensiveguidebook encompassing three chapters as Shelter, WASH, and Financial Literocy has been developed.

The collection and compilation of the information became possible only through continuous collaboration with grass root level

organizations, local Government authorities, Architects, and Engineers associations. Through the guidebook, we have addressed

the gaps and needs in the housing sector exclusiveluI Paravur TallJk which can sensitive and influence the policymakers for

furtherpolicy development in planning the positive changes in the shelter sector.

We envisage reaching out to all the individuals in Paravur creating awareness regarding Disaster Resi/ient Housing, common practices, methods, and suitable materials in house construction, various Govt. housing schemes, and so on. We, Habitat India and CDP hope that the /irst edition of the handbook on HSS in Paravur Taluk will become an essential /irststeppingstone towards creating a community with strength, stability, and self-reliance.This handbook can continue as a reference for comprehensive shelter, WASH, and Financial IiteracY ractiCes afid will be useful for years to come as it emphasizes on buildingdisaster resilient, healthy and selficient community

| Name | Contact | Name | Contact |

| Tahsildar and Village Offices | Contact Number of Collectors | ||

| Tahsildar Paravur | 0484-2442326 | District Collector | 0484-2423001 |

| Municipal Office | 0484-2442327 | Dy.Collector (Genl)/ADM | 0484-2422282 |

| Village Office, Vadakkumbhagam | 0484-2466332 | Dy.Collector (RR) | 0484-2422292 |

| Village Office, Alangad | 0484-2672658 | Dy.Collector (LR) | 0484-2422292 |

| Village Office, Chendamangalam | 0484-2518575 | Dy.Collector (LA) | 0484-2422292 |

| Village Office, Eloor | 0484-2547111 | Dy.Collector (election) | 0484-2422292 |

| Village Office, Ezhikkara | 0484-2508859 | Akshaya District Office | 0484-2422693 |

| Village Office, Parur | 0484-2440438 | Agricultural Development & Farmers Welfare Department Contact Details | |

| Village Office, Kadungalloor | 0484-2609575 | ADA Paravur | 0484-2448664 |

| Village Office, Kottuvally | 0484-2440437 | Kottuvally | 0484-2440207 |

| Village Office, Kunnukara | 0484-2479980 | Chendamangalam | 0484-2518122 |

| Village Office, Karumaloor | 0484-2672659 | Vadakkekara | 0484-2440204 |

| Village Office, Moothakunnam | 0484-2484432 | Chittattukara | 0484-2440334 |

| Village Office, Puthenvelikara | 0484-2487250 | Paravur Municipality | 0484-2440194 |

| Village Office, Vadakkekara | 0484-2440439 | Ezhikkara | 0484-2508095 |

| Village Office, Varapuzha | 0484-2511652 | Town Employment Exchange North Paravur | 0484 2440066 |

| Helpline Numbers – Government of Kerala | |||

| Taluk Supply Officer, North Paravur | 0484 2442318 | Chief Minister’s Distress Relief Fund | 0471-2518513 |

| Child Helpline | 1098 | Consumer Toll Free Helpline | 18004251550 |

| Women Helpline | 1091 | CPC Call Center | 1800-425-2229 |

| Crime Stopper | 1090 | Disaster Management Helpline | 1077 |

| DIAL A DOCTOR | 1056 | Highway Alert | 9846 100 100 |

| Call Center for General Query | 1961 | KSRTC Helpline | Tel: 0471 – 2463799 |

| Election Helpline | 1950 | KSEB | 1912 |

| Pink Police Patrol | 1515 | Labour Call Centre | 1800 425 55214/ 155215 |

| Citizens Call Centre | 155300 | Pradhan Mantri Jan-Dhan Yojana (PMJDY) | SLBC Call centre: 1800 425 11222 |

| Labour Minister’s Helpline | 155 300 | PWD Helpline | 1800 425 7771 |

| Rail Alert | 9846 200 100 | State Consumer Helpline | 1800-425-1550 (Toll free) |

| Ration card renewal | Tel: 0471-2320379, 9495998223 | UID/Aadhaar | 1800-4251-1800 |

Financial Literacy for Financial Inclusion

As per a global survey by Standard & Poor’s Financial Services LLC (S&P) less than 25% of adults are financially literate in South Asian countries. For an average Indian, financial literacy is yet to become a priority. India is home to 17.5% of the world’s population but nearly 76% of its adult population does not understand even the basic financial concepts.

The survey confirms that financial literacy in India has consistently been poor compared to the rest of the world. Financial illiteracy puts a burden on the nation in the form of higher cost of financial security and lesser prosperity. An example of this is the fact that most people resort to investing more in physical assets and short-term instruments, which conflicts with the greater need for long-term investments, both for households to meet their life stage goals and for meeting the country’s capital requirements for infrastructure.

In India, there are also certain erroneous beliefs associated with financial literacy, the most common being the myth that one who is ‘literate’ or ‘rich’ is also ‘financially literate’. Lack of basic financial understanding leads to unproductive investment decisions. Another myth is that financial literacy is more important for adults. We can achieve the desired results from financial literacy only when we start educating our children. Like many other provocative topics, money is something that kids hear about outside homes as well, which exposes them to wrong perceptions.

Financial regulators in India — Reserve Bank of India (RBI), Securities and Exchange Board of India (Sebi), Insurance Regulatory and Development Authority of India (Irdai) and Pension Fund Regulatory and Development Authority (PFRDA) — have created a joint charter called ‘National Strategy for Financial Education on detailing initiatives taken by them and also other market participants like banks, stock exchanges, broking houses, mutual funds and insurers. What is required is a joint effort by all the banking, financial services and insurance companies as well to be able to achieve noticeable changes in the perceptions that an average Indian has about financial management.

The recent mammoth exercise of demonetization should help bring many more people into the organized sector, thereby opening up possibilities for financial inclusion and literacy. The launch of digital wallets, Universal Payments Interface (UPI) and new-age commercial and payments banks have paved new ways for a less-cash economy. The push to increase usage of mobiles for payments is significant, as India is already the world’s second biggest smartphone market with over 220 million smartphone users. These numbers create enormous possibilities to go digital and create new opportunities to engage and share financial knowledge with consumers.

Financial literacy and financial stability are two key aspects of an efficient economy. Financial literacy enhances individuals’ ability to ensure economic security for their families. In India, on one hand, there is a need to reach out to lower income groups and economically weaker sections, and on the other, to millennials who are hyper- connected and require tailor-made financial products but have limited awareness of the possible financial solutions.

Housing Sanitation and Financial Literacy

According to the 2011 Census, there were 1.77 million homeless people in India, or 0.15% of the country’s total population. There is a shortage of 18.78 million houses in the country (as per 2011 census). Similarly, India, the world’s second-largest country by population, has the highest number of people (732 million) without access to toilets, according to a new re port by Water Aid, titled Out Of Order. It further stated that 355 million women and girls lack access to a toilet. The report also explains open defecation and lack of toilet facility as a major cause for stunting, diarrhoea deaths and anaemia mainly among children below five years of age.

Following are few government schemes under Ministry of Housing and Urban Poverty Alleviation (MoHUPA) for marginalized poor in India to get financial support to build and own house or build own individual household toilets but very few people have awareness on these schemes. Very few of them know about processes and procedures to get access to these schemes. There is a need to create awareness on these opportunities and empower laymen to get access to financial resources.

Pradhan Mantri Awas Yojana (PMAY)

The Pradhan Mantri Awas Yojana was launched by PM Narendra Modi in 2015. Also known as the Housing for All scheme, the mission is to provide shelters to the homeless by 2022. Under the scheme, the Centre would be providing assistance to states and UT to provide homes to every citizen within seven years. The Central government has also announced home loan interest subsidy to those who are buying their first home in urban areas. Under the scheme, the government will provide interest subsidy of three to four per cent for a home loan amount of up to Rs 9 lakh and Rs 12 lakh.

Rajiv Awas Yojna

Launched in 2009, the Rajiv Awas Yojana (RAY) envisages a slum-free India and encourages state and union

territories (UT) to bring all illegal constructions within a formal system. To increase the affordable housing stock under the scheme, the Centre

has approved the Affordable Housing in

Partnership (AHP) scheme to be part of the RAY. The scheme also provides support of Rs 75,000 per economically-

weaker sections (EWS), Dwelling Units (DUs) of the size of 21 to 40 sqm. So far, Rs 1,398 crore has been spent while 37,000 houses are being developed

under the scheme.

Pradhan Mantri Gramin Awaas Yojana

Earlier known as Indira Awas Yojna, the scheme focuses on providing pucca houses with basic amenities to homeless families. The objective is to build one crore homes of 25 sqm by 2022. The government shares the cost of construction with the state in the ratio of 60:40 in plain areas and 90:10 for north eastern and hilly areas. The cost for the unit assistance of Rs 1.2 lakh is also provided to the beneficiary.

People who will be benefitted are:

- Households without shelter

- Destitute/living on alms

- Manual scavengers

- Tribal groups

- Legally released bonded labour

Sanitation scheme for individuals

Ministry of Urban development provides Rs.4000 to construct a toilet with an additional incentive share from state government under Swatch Bharat Mission. Ministry of Drinking Water and Sanitation provides Rs.12000 as incentive per toilet for construction of individual household latrines. However, individual may need more funds to construct house or toilets as per his and his family priority or for additional services like water and electric connection, water tank fittings, construction of bathroom, tiles in the toilet, additional room or floor, colour or tiles in the house etc. For this one may seek help for financial assistance from different sources if he has knowledge on it.

What is Financial Inclusion?

Financial inclusion or inclusive financing is the delivery of financial services at affordable costs to sections of disadvantaged and low-income segments of society. An estimated 2.5 billion working age adults globally have no access to the types of formal financial services delivered by regulated financial institutions.

There are 5 important A’s in Financial Inclusion:

- Awareness

- Availability

- Accessibility

- Affordability

- Adequacy

What is MDI (Monthly Disposable Income)?

Disposable income is the amount of net income a household or individual has available to invest, save, or spend after deducting all expenses including income taxes, debts, liabilities, food expense, school fee, transport expenses, rent etc.

The formula is:

MDI=Net Family Income- Net Family Expenses

Saving:

The surplus money left with us from all sources of income after all the

expenses is called savings.

Investment:

When we save money and deploy that money in expectation that with time the money will give higher

returns is called investment

Debt:

When our expenses are more than our income them we will have no savings and as a result in times of

financial need we will borrow money from individual or institution, this creates debt

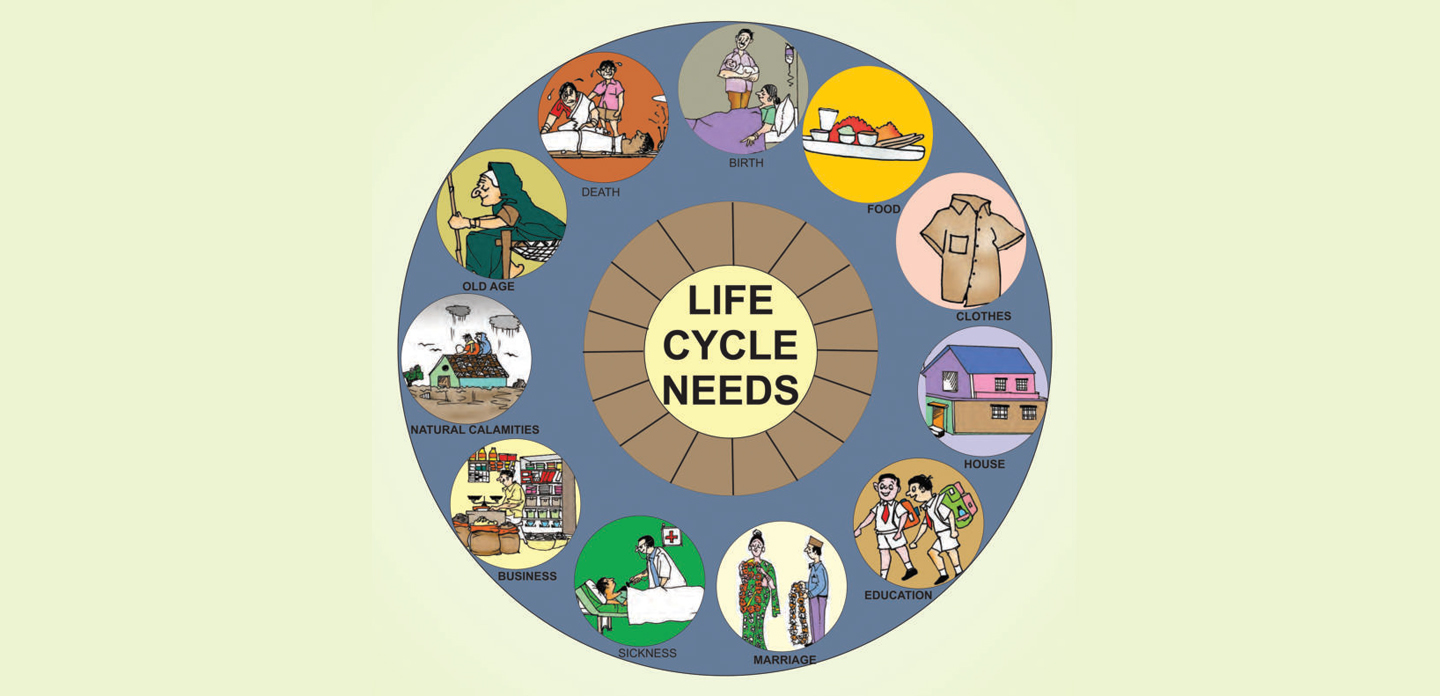

WHY to save:

look at the picture below, it depicts our life cycle which goes

through various expected and unexpected changes, incidents and events. Every incident or change brings financial burden and one need

to be prepared to meet such expenses else they will have to borrow money and fall in the trap of debt.

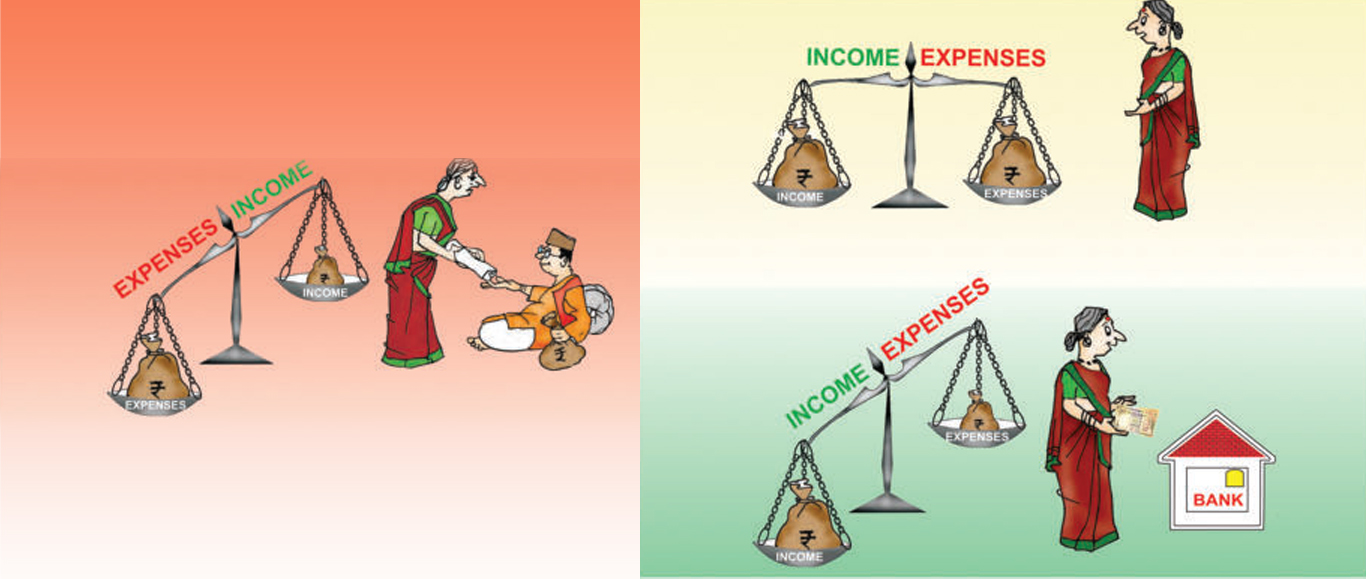

How to manage debt?

By managing the balance between income and expenses, we can avoid falling in the trap of debts. If we learn not to spend more than our income we can save money and invest in bank or other options for savings. This way, we can get more returns for our money over a period of time or we can use this money at the time financial crisis instead of borrowing with high interest.

Close

Close

Financial Planning

Taking care of income and expense balance carefully is called financial planning. Let’s understand the picture on essential and non-essential expenses. There are expenses which are mandatory like food, cloths, housing , education, marriage, illnesses etc. but there are expenses which can be controlled like expenses on luxury items like excursions, eating out, parties, liquor or expensive hobbies etc. This way we can save some money to meet exigencies or pay debts. It’s like preserving or saving water for family in a pitcher.

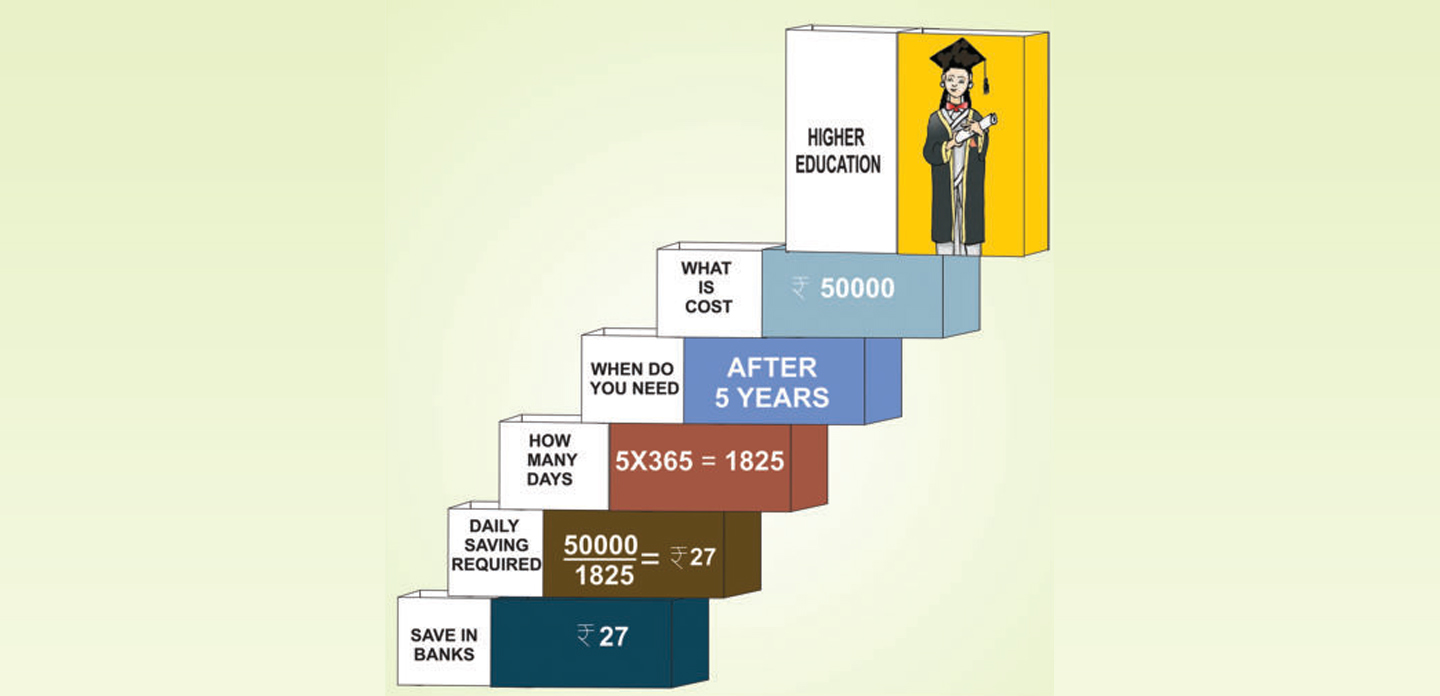

In financial planning we need to plan and determine family goals and then plan savings as well. For example, you want to save money for higher education of your daughter. In the picture the required amount and available time is calculated to understand necessary daily saving. The same can be calculated for months.

Financial diary

After determining the family and personal goals we can also maintain a financial diary to ease financial planning. The Vices can be avoided, Wants can be reduced and needs to be met but should always be limited.

Borrowing

In emergencies when our income is less than our expenses we tend to borrow debt from individuals, institutions and traditional money lenders. The stagnant income doesn’t give us any saving but this debt and associated interest increases burden of loan and repayment. If there is no saving plan and no financial planning, the burden of loan increases day by day,

Options for Borrowing

Banks are reliable, transparent and safe institutions and one should always opt to borrow from banks only. There are reliable and safe organisations at local level like SHGs, local NGOs and financial institutions that facilitate lending with banks. Such organisations not only help to get linked with bank but also provide required guidance and education so that you and money is always safe.

Borrwing for new houses, home improvement and sanitation facility

HFH India provides loan to construct new houses, improve existing houses and to construct toilet facilities, construct bathroom, construct water storing options etc. HFH India also helps to create linkages with banks and financial institutions to get loans. HFH India also has financial education facility for beneficiaries to understand loan, banking, functional literacy for micro financing etc.

Checklist for beneficiaries/end users: To understand housing/sanitation need

One needs to answer few questions before deciding on investing on housing or sanitation infrastructure:

Understanding need for sanitation/housing:

understand the need of your investment or saving? Owning a house is matter of social security, dignity and pride, similarly having own sanitation unit is a matter of privacy, dignity and well- being for the whole family especially women of family. Homeownership can offer many advantages including tax benefits, financial security and pride to own a house. However analyse if you really need to buy house or you are happy with rented house.

Analysing affordability for Housing/construction for sanitation: Analyse all your liabilities and expenses along with income sources. Can you afford monthly instalment with the rent you pay and you have sufficient savings possibilities. Are there options for you to increase family income to afford monthly instalment for long time. How stable is your monthly income and how that can be increased with supplement income or savings.

Incremental construction or progressive housing /Building in stages: You need to plan for construction as per Family’s available disposable income deducting all debts, liabilities, expenses and taxes. You can also plan for incremental construction or construction in stages, for which HFH India construction team can be contacted. The construction plan has to be thoughtful, technically sound and fit to budget and therefore, consultation of field expert is important.

Analysing Credit abilities: Try to understand your credit abilities, some banks and financial institutions do it free of cost. This will also help you to determine down payment for house buying or loan amount.

Tool for beneficiries to reach financial goal for sanitation/housing

There could be 10 steps to reach financial goals by client or beneficiaries:

-

Set financial priorities:

Take a while and understand your life style and spending pattern. Analyse what affects your spending and financial decisions and what are actual life/ family priorities.

-

Get organised:

Keep a track on your financial investments and savings along with daily check on income and expense. Keep a file for all financial documents like bank statement, credit card information, investment information, insurance policies, will papers etc., which is accessible, fire proof and safely secured. Some documents can be kept in safe deposit box at a bank for more safety like , birth certificate, death certificate, marriage license, divorce papers, copies of will etc.

-

Track your money:

Control your financial situations and expenses. Manage your bank, credit card expenses statements with actuals on a notebook.

-

Shop smarter:

- Make list of shopping trips and stick to needy items to avoid impulse purchases.

- Use cash for purchase instead of credit or debit cards and buy only for cash you have

- Buy from generic store brands at supermarkets.

- Compare prices and look for sales and off season bargains

- Buy in bulks, it saves money but don’t buy more than you realistically use

-

Review and reduce your debt:

Total consumer debt should be less than 20 percent of your net income. Consumer debt includes credit card payments, car loans, student loans and any other debts that you repay monthly, and does not include money spent on a mortgage, rent, utilities or taxes. Use these calculations to assess your debt load.

- My yearly net income after taxes and deductions is Rs……………….

- My monthly net income is Rs……………….(yearly income divided by 12).

- According to the 20 percent guideline, the amount of consumer debt per month that I should not exceed is Rs………………….(Monthly income x 0.20).

- Create a get-out-of-debt plan. Calculate how long it might take you to pay off your debt.

- Cut expenses. Try to identify a few things you could stop buying or buy less often.

- Get a second job/income source. Try to increase income. Is it possible to get a second job or overtime?

- Prioritize debts. Pay off the highest interest rate debts first and move funds to the next when paid off.

- Shift higher-interest loans to a single lower-interest loan.

- Stop running up new charges.

- Keep only one or two major credit cards and consider having the limits lowered.

- Set your goal. Each month, I can afford to pay around Rs. For my consumer debt.

-

Build a strong Credit Report:

Your credit report is a record of how you’ve paid your debts in the past. It shows the current amount of debt you have, and how much debt you’ve repaid.

-

Save for your future:

Saving money is not easy, but it is essential to achieving financial well-being and securing your future. One of the best and easiest ways to save money and start a strong retirement income planning program is to pay yourself first. Every time you receive a pay check, save a certain percentage of your income before spending money on anything else. You may choose to have your bank automatically transfer a certain amount of money from your account to your savings each month.

The Time Value of Money: The earlier we start saving, the more interest can be earned

Saving Versus Investing: Investing carefully is more lucrative and earns profit than only saving. Invest only in registered entities.

Saving for an Emergency: Emergency fund should be saved to meet exigency situations may be to cover basic living expenses for three to six months.

-

Set Financial Goals:

Set Long term, medium term and short term financial goals: Try to set SMART goals. These are goals that are Specific, Measurable, Achievable, Realistic and Time-Bound. Make sure you prioritize your goals. Which ones are the most important to you? Work toward achieving these goals first.

-

Create a spending Plan:

Putting your financial goals in writing can make them more concrete and achievable. However, it’s easy for everyday purchases and obligations to get in the way of saving for the future. One of the best ways to make sure your daily spending habits don’t overwhelm your life goals is to create a spending plan.

A spending plan is not meant to be a strict budget. Instead, it’s a guide that will help you take control of your financial future and, ultimately, reach your goals.

-

Invest money to reach your goals:

Once you’ve identified your financial goals and established a spending plan, you know what you’re saving for and how much you’ll need to get there. For longer-term objectives, investing is one of the best ways to watch your money grow.

When you invest, you put money aside for long-term goals such as retirement or a child’s education. The easiest way to do this is by having money automatically deducted from your bank account or paycheck and put into the investment vehicle of your choice.

Pradhan Mantri Awas Yojana (PMAY)

The Pradhan Mantri Awas Yojana was launched by PM Narendra Modi in 2015. Also known as the Housing for All scheme, the mission is to provide shelters to the homeless by 2022. Under the scheme, the Centre would be providing assistance to states and UT to provide homes to every citizen within seven years. The Central government has also announced home loan interest subsidy to those who are buying their first home in urban areas. Under the scheme, the government will provide interest subsidy of three to four per cent for a home loan amount of up to Rs 9 lakh and Rs 12 lakh.

Eligibility:

People belonging to the Economically Weaker Section (EWS), Low Income Group (LIG), Middle Income Group-I (MIG-I) and Middle Income Group-II (MIG-II) are eligible for this scheme. Age of the applicant must be 70 years or less Income range of the applicant must be below Rs. 3 lakhs per annum for economically weaker sections and between Rs. 3 – 6 lakhs per annum for lower income groups Women who are citizens of India are eligible

Beneficiary:

-

- They must meet the income requirement of the scheme.

- The beneficiary family should not already own a ‘pucca’ house anywhere in India under their own name.

- The beneficiary family should not have already availed any other central assistance under any housing scheme from the Government of India or benefit under any scheme in Pradhan Mantri Awas Yojana (PMAY).

- The beneficiary family shall comprise of husband, wife and unmarried children. However, under the MIG category, an adult earning member irrespective of his/her marital status can also be treated as a separate household.

- For married couples, either spouse or both of them together in joint ownership can be eligible for a single subsidy.

Exception:

An adult earning member (irrespective of marital status) can be treated as a separate household – which means a bachelor availing a loan can also avail subsidy if he/she is buying property in his/her name.

Coverage:

All Statutory Towns as per Census 2011 and towns notified subsequently will be eligible for coverage under the Scheme.

How to apply?

The borrower can apply for the Housing Loans and CLSS subsidy through the PLIs (Prime Lending Institutions, banks etc.). This institutions/banks perform due diligence and check the fulfilment of the eligibility criteria for the scheme, then the required criteria are satisfied they submit the borrowers claim to Central Nodal Agency (CNA). The CNA processes the claim and releases the subsidy amount through that institute/bank. The institute/bank adjust the same by crediting to the borrower’s Loan account resulting in reduced loan outstanding and the effective EMI.

Key features

- Interest subsidy of 6.50%* p.a. up to a loan amount of D6 lakh for 20 years or the actual term, whichever is lower, credited upfront

- Actual subsidy amount credited is as approved by the National Housing Bank (NHB)

- Family means husband/wife/unmarried children

- Applicable for customers who are purchasing/constructing their first home. The beneficiary family should not own any other house in their name.

- The carpet area should not exceed 30 sq. mt. for EWS (annual household income up to Rs. 3 lakh PA), 60 sq. mt. for LIG (annual household income between Rs. 3 lakh to Rs. 6 lakh PA), 120 sq. mt. for MIG-I (annual household income between Rs. 6 lakh to Rs. 12 lakh PA), and 150 sq. mt. for MIG-II (annual household income between Rs. 12 lakh to Rs. 18 lakh PA)

- The construction/extension must be completed within 36 months

- A woman has to be owner/co-owner of the property